Overview

“Accrual accounting is the heart and soul of corporate financial

reporting. It encourages companies to make estimates of a wide variety of key

financial variables and allocate revenue to specific quarters or periods of

time. Accrual accounting allows companies a great deal of flexibility, which is

appropriate. But it can also be a problem. Too many companies are taking

advantage of that latitude to push their estimates to the limits in order to boost

earnings. Most of it is perfectly legal, but that's no solace to investors who

are left to decipher hidden, confusing assumptions and judgments made in

reported earnings. Despite all the recent accounting reform, more work remains

to be done. Companies have to clean up their financial statements to give

investors transparent and consistent financial data or prepare to be punished

in the market. Wall Street is already catching on to the shenanigans on income,

balance-sheet, and cash-flow statements.” --- Business Week, OCTOBER 4, 2004, The New Earnings

Game

Accounting accruals represent non-cash

accumulations and can affect all four major accounting statements. Measuring these accumulations at the end of

an accounting period results in balance sheet items such as “Accounts

Payable,” “Accounts Receivable,”

“Deferred Taxes,” and “Goodwill.” The

other side of these account balances are income statement entries such as

“Accrued expenses,” “Accrued Revenues,” “Tax Expense,” and “Amortizations” that

are recognized by applying the matching

principle.

Accruals are of interest

to investors, because as you will learn in this lesson, they can relate to both past and estimated future cash

flows. In the academic research

literature, the famous “accruals anomaly” has placed accruals on center stage. The research showed that if you decompose accounting

income into accruals and cash income, you find that these components have

different implications for forecasting future income. This means you have to pay attention to

accruals separately from cash income.

Understanding Accounting Accruals

The difference between

“Accounting Income” and “Cash Income” result from accruals. The income statement is where you see

accounting accruals and their impact upon the measurement of revenues, gains,

expenses and losses. Operationally this

results from applying the matching principle

which binds together revenue and expense recognition over a period of time.

A quick history: this approach to accruals was popularized in the 1940 American

Accounting Association monograph by Professors W.A. Paton and A.C. Littleton’s

“An Introduction to Corporate Accounting Standards.” This monograph provided a comprehensive

rationale for historical cost accrual accounting, including highlighting the importance

of the matching principle. In this

monograph the accounting income statement received primary focus and the

balance sheet was treated as the residual of the income statement. Subsequent

to Paton and Littleton’s monograph fair value accounting and a second concept

of income, comprehensive income, evolved.

These developments resulted in the balance sheet also being recognized

as a primary driver of accruals that by-passed the Income Statement. This resulted in SFAS 130, Reporting of

Comprehensive Income, in 1997 establishing reporting standards in response to

these developments.

The objective of this

lesson is to become familiar with accounting accruals as applied in practice,

including providing an introduction to understanding the subtle relationships

between accruals and cash flows, and particularly how different accruals result

from both past and estimated future cash flows.

In the next section we

will exploit these developments by starting with Paton and Littleton’s income statement

insights within the context of the indirect form of the cash flow

statement. This treatment is then extended

to the Statement of Stockholders’ Equity to cover accruals that bypass the

accounting income statement.

Identifying Accounting Accruals: A Consolidated Cash Flow Statement Approach

The Consolidated

Statement of Cash Flows for companies that use the indirect method, provide a natural

starting place for learning about accruals.

This is because this statement reconciles opening and closing cash

balances by starting with the Accounting or Net Income and then undoes the adjustments

resulting from accrual accounting to get back to an estimate of cash

income. Further, these adjustments are

classified by activities (Operating, Investing and Financing) to provide

investors with additional information.

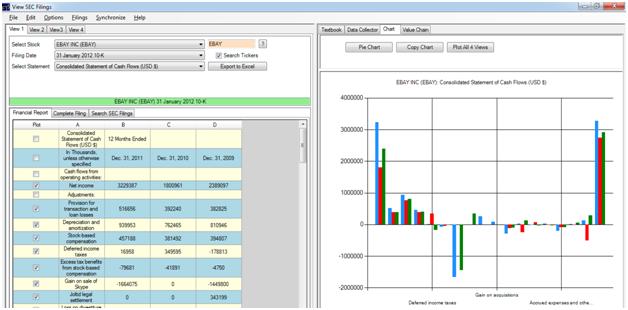

Consider EBAY for

adjustments related to Operating Activities.

Working from Left (Net Income) to Right (Net Cash Provided by Operating

Activities) in the screen below it is immediately apparent that EBAY has made a

number of adjustments. The bar chart

reveals the relative significance of each adjustment.

As a result, we will

first focus on sub sets of the accrual adjustments in this statement for EBAY.

Accruals at Work

Some major news for EBAY

in 2011 was the sale of Skype to Microsoft:

Accounting Accruals at Work: Skype, Cash Flows and Accounting Accruals

To see how accounting

accruals resulting from this transaction permeates through the accounting

reports consider first the Consolidated Cash Flow Statement which EBAY present

in indirect form. The Skype transaction was

for cash so it reflects a combination of accrual and non-accrual entries that influence

two parts of this statement: Cash Flow from Operating Activities and Cash

Flows from Investing Activities.

Recall a cash flow

statement is reconciling the opening and closing cash balance starting with

accounting net income. As a result, the

sale of Skype has a large gain associated with it in accounting net income plus

Microsoft paid cash for Skype so the cash account has to reflect EBAY’s share

which was in excess of 2-billion dollars.

How are these entries

reflected in this statement?

The accrual part of the

transaction is reflected in the gain, relative to the book value, from the sale

of Skype in accounting Income and the non-accrual part is the in excess of $2

billion cash received by EBAY from Microsoft.

Accrual Adjustment

The

above reveals a large negative adjustment to Operating Activities (circled in

red). This is undoing the effects of the

gain from this non re-occurring sale from operating activities, that is in the

Net Income number for the year.

Cash Adjustment

The Sale of Skype was for cash as

presented in the above news story and so the larger addition to Investing

Activities circled in blue reflects the accounting for the sale.

It is further observed that the gain

adjustment is less than the cash adjustment because the gain is net of the book

value. This also illustrates the

importance for an analyst to check whether a sale of an investment is for cash

or some combination of cash and stock.

Additional Accrual Adjustments: Past versus Future Cash Flows Effects

Many other accrual adjustments are

one-sided in relation to the Indirect Form of the Cash Flow Statement (i.e.,

Income Statement). That is, the

corresponding impact is on the Balance Sheet.

Consider the following set of EBAY adjustments:

For EBAY the change in Accounts

Receivable is a use of funds as Accounts Receivable have increased. Accounts Payable is a source of cash (because

payments have been delayed). The above

also reveals that Accrued Expenses and Other Liabilities have been a use of cash. The residual of these activities is on the

Balance Sheet in the following form:

Here the corresponding Balance Sheet

activity is consistent for Accounts Receivable – that is, increase in accounts

receivable over the year is a use of cash funds. Similarly, Accounts Payable is consistent

that is an increase in the Accounts Payable current liability is a source of

cash funds. The only strange activity in

the above is that “Accrued expenses and other liabilities” is a use of cash on

the Cash Flow Statement in the Consolidated Cash Flow Chart but it is also an

Increase in Liabilities on the Consolidated Balance Sheet. On the surface this is an inconsistent

treatment of accruals. This is because

Accrued Expenses suggests that the expenses have not been paid in cash but they

have been recognized on the income statement.

This would trigger an add-back because it is non-cash expense. However, the cash flow adjustment is the

opposite it is a decrease even though the Balance Sheet liability

increases.

This underscores the complexities

that face an analyst when attempting to disentangle accrual adjustments because

accruals are combined with aggregations. In these cases one looks to the footnotes for

clues regarding how to resolve these conflicts.

Good reporting will provide sufficient information in the footnote disclosures

even though this may be rather cryptic at times.

The one clue to the above EBAY

puzzle is the following footnote in relation to this Balance Sheet item:

“In the second quarter of 2011, we

settled multiple uncertain tax positions resulting in an overall decrease in

our unrecognized tax benefits. As of December 31, 2011, our liabilities for

unrecognized tax benefits were included in deferred and other tax liabilities,

net. As of December 31, 2010, $208.5 million of our liabilities for unrecognized

tax benefits were included in accrued expenses and other current liabilities

and the remaining amount is recorded as deferred and other tax liabilities.”

In other words EBAY has aggregated some sizeable non cash

tax related numbers into this balance sheet item (Accrued Expenses and Other

Current Liabilities) that pertained to tax benefits not recognized in

2010. If these benefits were recognized

in 2011 then this would explain why Accrued Expenses and Other Liabilities

results in a deduction in the EBAY’s cash flow statement. That is, the non-cash gain is subtracted out

of Net Income as an accrual adjustment. The Cash Flow Statement graph above is

consistent with this treatment. The

treatment for 2011 appropriately places additional tax benefits in the

“Deferred and Other Tax Liabilities” account for 2011 which reflects an

increase.

The cumulative effect of these tax adjustments end up in the

Provision for Income Taxes. This

provision can have a significant impact upon accounting accruals because it

does not equal the taxes actually paid.

Accruals that By-Pass the Income Statement: Other Comprehensive Income

There is an additional set of

accruals that do not affect the Income Statement. These arise primarily from Hedging

Activities, Unrealized Gains and Losses arising from Available-for-Sale

securities, Foreign Currency Translations and Defined Benefit Pension

liabilities. Although these items do not

impact Accounting Net Income they do impact the concept of Comprehensive Income

via a stockholders’ equity account referred to as “Other Comprehensive Income.”

For EBAY the current year’s accrual

adjustments for EBAY that impact Other Comprehensive Income are depicted below:

Given these are unrealized they will

not impact the income statement but instead will impact different parts of the

Consolidated Balance Sheet. However,

these items do have significant implications for financial analysts and

investors who are interested in forecasting current and future cash flows from

accruals.

Summary

Accounting accruals as Paton and

Littleton in 1940 observed are driven by the impact from the matching principle

which binds together revenues and expenses on the accounting income

statement. This in turn results in

accounting income not equaling cash income.

Today accruals are further driven by accounting developments subsequent

to Paton and Littleton such as fair value accounting and the concept of

comprehensive income. These concepts have

elevated the Balance Sheet to also being a driver of accruals because no longer

can this statement be viewed in the Paton and Littleton sense as purely the

residual of the income statement.

Investors and analysts are interested in accruals because by decomposing

accounting income into accruals plus cash income these two components behave

differently when used to predict future income.

This difference versus the market’s assessment of this difference lies

at the heart of the accruals anomaly.

0 comments:

Post a Comment