Overview

Cost Volume Profit is an

important managerial and financial analyst tool for understanding the operating

risk faced by a firm. Suppose management

and analysts want to answer the following types of questions:

How much does each $ of sales revenue contribute to the bottom line on average?

How sensitive is the bottom line (i.e., corporate P&L) to a downturn in sales from recession?

How can management and

analysts assess the expected return from a company’s sales and marketing

investing strategy?

You can answer these

types of questions and more, from a Cost Volume Profit analysis.

The starting point is to

first evaluate cost behavior in terms of the following simple equation:

Total Cost

(TC) = Variable Cost per Unit of Activity (VC) * Activity + Fixed Costs (FC) 1)

The above is useful for both assessing profitability as well

as assessing risk. For example, this

linear function underlies standard activity analysis where profit and loss is

projected for different levels of activity. For example, an analyst needs to forecast

future earnings and can approach this problem by applying standard CVP analysis

or as it is also referred to “Activity Analysis.” This is because from an outsider’s

perspective the natural choice of “activity” is Sales Revenue. Furthermore, if sales revenue growth can be

predicted and cost behavior can be estimated, an analyst can forecast

earnings. Given the increased importance

of “Earnings Season” in the capital markets this tool assumes additional

importance.

Important Aside

The above equation

assumes that the scale of operations remain unchanged which is usually not the

case for a growing firm as revealed from their investing activities (measured

in the cash flow statement). When this

is the case then an additional adjustment is required to “FC” in equation 1) to

account for the increased level of investing activities resulting in increased

Fixed Costs (FC) when projecting future earnings.

Implementing Cost Volume Profit Analysis

For CVP analysis we need

to estimate the % of each cost category that is variable. That is, if $100 is COGS what is the %

variable and what is the % fixed?

Equation 1) does not

answer this second question. Assuming

the unit of activity is $ sales revenue then VC is a % of Sales Revenue but not

a % of the cost category. To compute the

% of the cost category we apply the following transformation:

%

Variable Cost for a specific Category = (VC*Sales/Cost Category)*100 2)

Applying CVP Analysis

In this lesson we will

assume that Sales Revenue is the unit of activity.

Step 1: Estimating the Variable Cost per $ of Sales

Revenue

There are three main approaches

to assessing cost behavior. These

approaches are:

Account Analysis and

Professional Judgment

High-Low Cost Method

Regression Analysis

In practice an analyst

will employ all three techniques.

Step 2: Transform the estimate into a relative % for each cost category.

Account Analysis and Professional Judgment

First, Account Analysis

is always the starting place. Here

understanding the business model and the relative makeup f the balance sheet is

important. For example, COGS for a retailer

is going to have a large variable proportion to it even if you know some fixed

costs are allocated to COGS. The simple

reason being the higher the turnover the larger the dominance the variable cost

drivers will be in COGS. As a result,

for a retailer it is not unusual to assume between 90-100% variable. Similarly, for business that does not have a

large amount of fixed assets on their balance sheet.

For example, contrast

the latest Balance Sheets for Microsoft and Intel (using Valuation Tutor’s data

collector and plotting abilities):

It is immediately clear

that Property Plant and Equipment is of far more importance to Intel’s business

model than it is to Microsoft.

As a result, estimating

the % of cost of goods sold that is variable usually require going beyond the

professional judgment approach.

Estimating Cost Behavior Relative to Sales for

COGS

The easiest technique to

apply is the High/Low method. This will

give a reasonable estimate. For the case

of Intel, by examining two recent 10-K’s and using the data collector, we can

collect four or five past observations:

In the above example, we

have collected all cost categories down to Operating Income for Intel from

their 2012 10-K and their 2010 10-K.

Note: for some firms you

may need to work with their 10-Q’s.

By double clicking on

any line item in the LHS of the screen automatically transmits to the RHS so it

is easy to work across statements. When

done click on Copy All (Button RHS of screen), Paste into Excel and Clean Up to

get:

Operating expenses is

the sum of Research and development, Marketing, general and administration,

Restructuring and Amortizations.

Hi Lo Method

This method uses

observations on two dates to estimate fixed costs and the variable cost per

dollar of sales revenue. The Y-Axis

variable is the aggregate cost category and the X-axis variable is the volume

of activity (sales revenue for a financial analyst).

Variable

Cost Per $ Sales Revenue = (Total Costs

High Sales Revenue – Total Costs Low Sales Revenue)/(Sales Revenue High – Sales

Revenue Low)

Working with the above

Intel Data the Hi/Lo method reveals:

That is, the Variable

Cost per $ of Sales for Intel’s Cost of Sales equals 0.1157.

Question: What is the cost behavior equation?

The beauty of the hi/lo

technique is that you can solve for FC from by substituting in one of the two

points:

Total Cost (TC) = Variable Cost per Unit of Activity (VC) * Activity

+ Fixed Costs (FC)

53,999 = 0.1157*20,242 + FC => FC = 13,994.

Regression Analysis:

One advantage of running

a simple regression is that we now use all observations not just the high and

the low. Running regression we get a

little higher estimate for the Variable Cost per Dollar of Sales at: 0.185 and

a lower fixed cost estimate of $9496.

In both cases this is

well below the case for a retailer or a software company.

Working with the

regression analysis then the % variable costs for COGS is 18.5% and 81.5%

fixed.

Results from Cost Behavior Analysis:

Columns 2 and 3 contain

the results from Hi/Lo for all cost categories and columns 4 and 5 the

regression analysis. Columns 2 and 4

contain the estimate of the variable cost per dollar of sales and columns 3 and

5 the implied Fixed Costs from the analysis.

Observation 1: When the implied fixed costs are negative

this is consistent with the model being miss-specified and so it is clear that

this happens less with the regression analysis versus the Hi/Lo the former

which processes more information to arrive at the estimate. In practice an analyst will combine their

professional judgment with statistical techniques such as regression analysis

to arrive at their final estimates for cost behavior.

A second important

point, especially when working across firms, is to impose some standard cost

categories upon the analysis. In

Valuation Tutor these cost categories are:

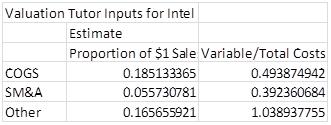

COGS, Sales, Marketing and Administration and Other. So for Intel our estimates for these three

categories are:

Other is based upon on

Research and Development which dominates this category for Intel. Given the projected proportion is greater

than one we will apply this as 100% variable and 0% fixed. This is consistent with the fact that

Research and Development is budgeted as a percent of sales.

The relationship between

the 2nd and 3rd columns above is that column 2 comes

directly from the Total Cost Equation that can be estimated from regression

analysis or applying the hi/low method to estimate the straight line. That is, column 2 is expressed relative to

the level of activity (i.e., % of sales).

Column 3 is the coefficient transformed to re-express the variable cost

component relative to the cost category directly as opposed to being a % of

Sales. The relationship between the two

columns are:

Variable/Total Costs =

Proportion of the costs relative to $1 Revenue * (Sales Revenue/Total Costs for

the Cost Category (e.g., COGS)).

0.4939 =

0.1851*(53,999/20,242)

In other words, the proportion

of variable costs to the total cost category will be higher than variable cost

per $ of sales estimated from a traditional regression analysis.

It is noted that the

inputs into Valuation Tutor are in the form of the third column, the proportion

of variable to the total costs in each category. This is because although a user may estimate

this from a regression it is also common to do this by employing account

identification/professional judgment.

Working with the Above Assessments: Variable versus Full Costing Income

Statements

In the screen shot below

the Valuation Tutor calculator is provided for Intel. Two income statement formats are

provided.

The two formats differ as

follows, in relation to Net Income from Operations (Illustrated for INTC in

millions for year ending Dec 31, 2011):

Absorption Costing:

Sales

(53,999)

Less

COGS (20,242)

Gross

Margin (33,757)

Less

Marketing and Administration (7,670)

Less

Other (8610)

Net

Income from Operations (17,477)

Now given our earlier estimates for

the proportion of variable costs for each expense line item provided earlier:

Other is based upon on

Research and Development which dominates this category for Intel. Given the projected proportion is greater

than one we will apply this as 100% variable and 0% fixed. This is consistent with the fact that

Research and Development is budgeted as a percent of sales.

The relationship between

the 2nd and 3rd columns above is that column 2 comes

directly from the Total Cost Equation that can be estimated from regression

analysis or applying the hi/low method to estimate the straight line. That is, column 2 is expressed relative to

the level of activity (i.e., % of sales).

Column 3 is the coefficient transformed to re-express the variable cost

component relative to the cost category directly as opposed to being a % of

Sales. The relationship between the two

columns are:

Variable/Total Costs =

Proportion of the costs relative to $1 Revenue * (Sales Revenue/Total Costs for

the Cost Category (e.g., COGS)).

0.4939 =

0.1851*(53,999/20,242)

In other words, the proportion

of variable costs to the total cost category will be higher than variable cost

per $ of sales estimated from a traditional regression analysis.

It is noted that the

inputs into Valuation Tutor are in the form of the third column, the proportion

of variable to the total costs in each category. This is because although a user may estimate

this from a regression it is also common to do this by employing account

identification/professional judgment.

Working with the Above Assessments: Variable versus Full Costing Income

Statements

In the screen shot below

the Valuation Tutor calculator is provided for Intel. Two income statement formats are

provided.

The two formats differ as

follows, in relation to Net Income from Operations (Illustrated for INTC in

millions for year ending Dec 31, 2011):

Absorption Costing:

Sales

(53,999)

Less

COGS (20,242)

Gross

Margin (33,757)

Less

Marketing and Administration (7,670)

Less

Other (8610)

Net

Income from Operations (17,477)

Now given our earlier estimates for

the proportion of variable costs for each expense line item provided earlier:

What are the immediate advantages from recasting the above in this way?

The immediate answers to this are

summarized as follows. A user can

immediately pull off the following set of performance measures:

Contribution

Margin Ratio = Contribution Margin/Sales Revenue

Contribution

Margin Ratio = (Sales Revenue – Total Variable Costs)/Sales Revenue

Break

Even (B/E) Analysis ($Sales Revenue) =

Total Fixed Costs/(Contribution Margin Ratio)

Break

Even (B/E) Margin = B/E $Sales Revenue/$Sales Revenue

For Intel these are:

Conclusions

Cost Volume Profit is an

important managerial and financial analyst tool for understanding the operating

risk faced by a firm. Some of the

important questions answered from this analysis are:

How much does each $ of

sales revenue contribute to the bottom line on average?

How sensitive is the

bottom line (i.e., corporate P&L) to a downturn in sales from recession?

Alternatively,

What is the current

Margin of Safety? Is this improving or

deteriorating?

When we connected the

dots across financial statements in an earlier lesson the potential importance

of investing in sales and marketing became apparent.

How can management and

analysts assess a company’s sales and marketing investing strategy?

Here again CVP analysis

provides powerful insights to be gained into these types of questions. For example, if the company spends $x on a

marketing campaign that is expected to increase sales revenue by y% what type

of return is this likely to generate and does this return cover the initial

investment cost of the marketing campaign?

The answer to this

question requires performing a cost versus benefit

analysis where the expected benefit is measured from the contribution margin

associated with the projected increase in sales.

0 comments:

Post a Comment